Will Roth Conversions REALLY Save You Taxes?

May 15, 2026

Two intelligent people can look at the exact same Roth conversion analysis and come to completely opposite conclusions.

And both of them can be right.

At the heart of almost every Roth conversion decision is one question:

Will this actually save me taxes?

That sounds like a simple question. But once you start accounting for all the moving pieces in a real retirement plan, the answer can become far more complicated than most people expect.

Before we go any further, there are other reasons to do Roth conversions besides simply lowering lifetime taxes. Roth conversions can help with tax diversification, widow’s penalty planning, future tax uncertainty, estate planning, and leaving behind more tax-efficient assets.

But in this article, I want to focus specifically on how to evaluate whether a Roth conversion actually saves money on taxes.

Key Takeaways

- Most Roth conversion analysis is incomplete if it only compares federal tax brackets.

- The real analysis should include the all-in tax cost, including IRMAA and the Net Investment Income Tax when applicable.

- Annual tax comparisons are useful, but cumulative tax burden over time is much more decision-useful.

- The timing of the break-even point matters. A strategy that saves taxes at age 94 may not feel very attractive.

- Future tax savings should be evaluated with the time value of money in mind.

- Tax savings alone should not be the only factor used to decide whether a Roth conversion is worthwhile.

Step 1: Calculate the All-In Tax Cost

Doing or not doing Roth conversions will absolutely affect your federal income taxes. If you live in a state that taxes income, it may also affect your state income taxes.

But that is not the full picture.

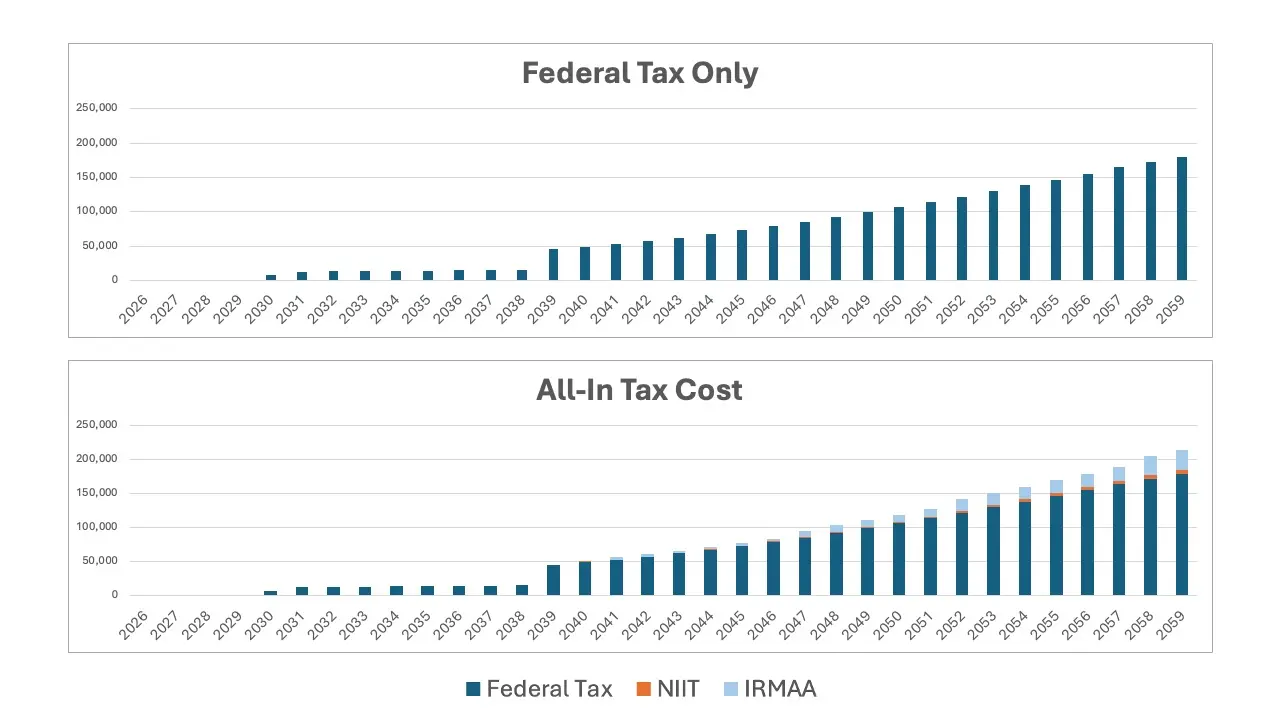

There are other costs tied to income too. Two of the biggest are the Net Investment Income Tax and higher Medicare Part B and Part D premiums through IRMAA.

The all-in tax cost of a Roth conversion may include:

- Federal income taxes

- State income taxes

- IRMAA surcharges on Medicare Part B and Part D

- Net Investment Income Tax

- Possible ACA premium subsidy impacts before Medicare age

- Other income-sensitive tax or premium effects

Why IRMAA Matters

IRMAA stands for Income-Related Monthly Adjustment Amount. In plain English, it is an additional Medicare premium that higher-income retirees may pay for Medicare Part B and Part D.

A Roth conversion increases your modified adjusted gross income in the year of the conversion. That can push you into a higher IRMAA bracket, which may increase Medicare premiums in a future year.

That does not automatically mean the Roth conversion is a bad idea. It simply means the IRMAA cost should be included in the analysis.

Why the Net Investment Income Tax Matters

The Net Investment Income Tax, often called NIIT, is a 3.8% tax that can apply to certain investment income, such as dividends and capital gains, once income crosses certain thresholds.

A Roth conversion itself is not net investment income. But because a Roth conversion increases modified adjusted gross income, it can cause more of your investment income to become subject to NIIT.

That is another reason a federal-tax-only Roth conversion analysis can be incomplete.

Once you include these additional costs, you can compare the strategies side by side and see how the tax burden changes over retirement.

In a no-conversion scenario, taxes may start relatively low. But once Required Minimum Distributions begin, federal taxes can climb quickly. Over time, IRMAA costs and the Net Investment Income Tax may grow too.

In a conversion scenario, the tax burden may be much higher upfront. But if the conversion reduces future RMDs, the tax burden may drop significantly later in retirement. In some plans, IRMAA may become much less of an issue after the conversion years are complete.

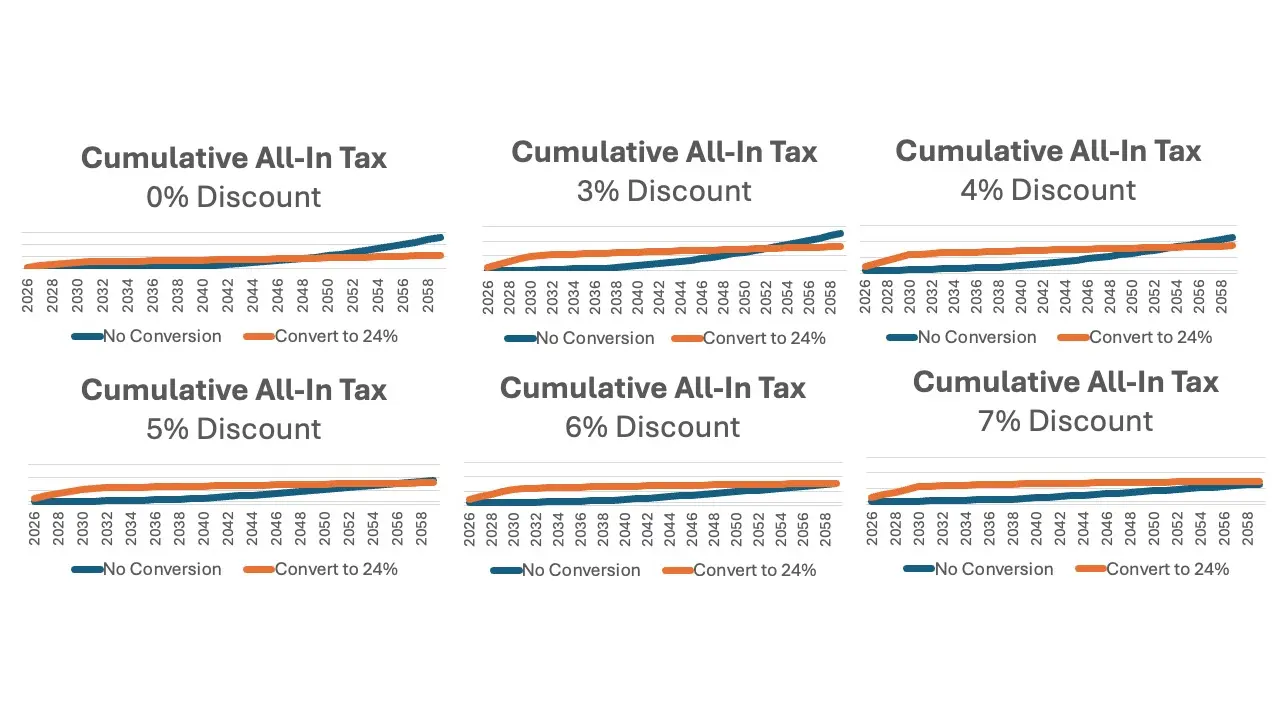

Step 2: Look at the Cumulative Tax Burden

Annual tax charts are useful, but they are still only snapshots.

To make a better decision, you need to look at the all-in tax burden on a cumulative basis over time.

There are two ways to do this.

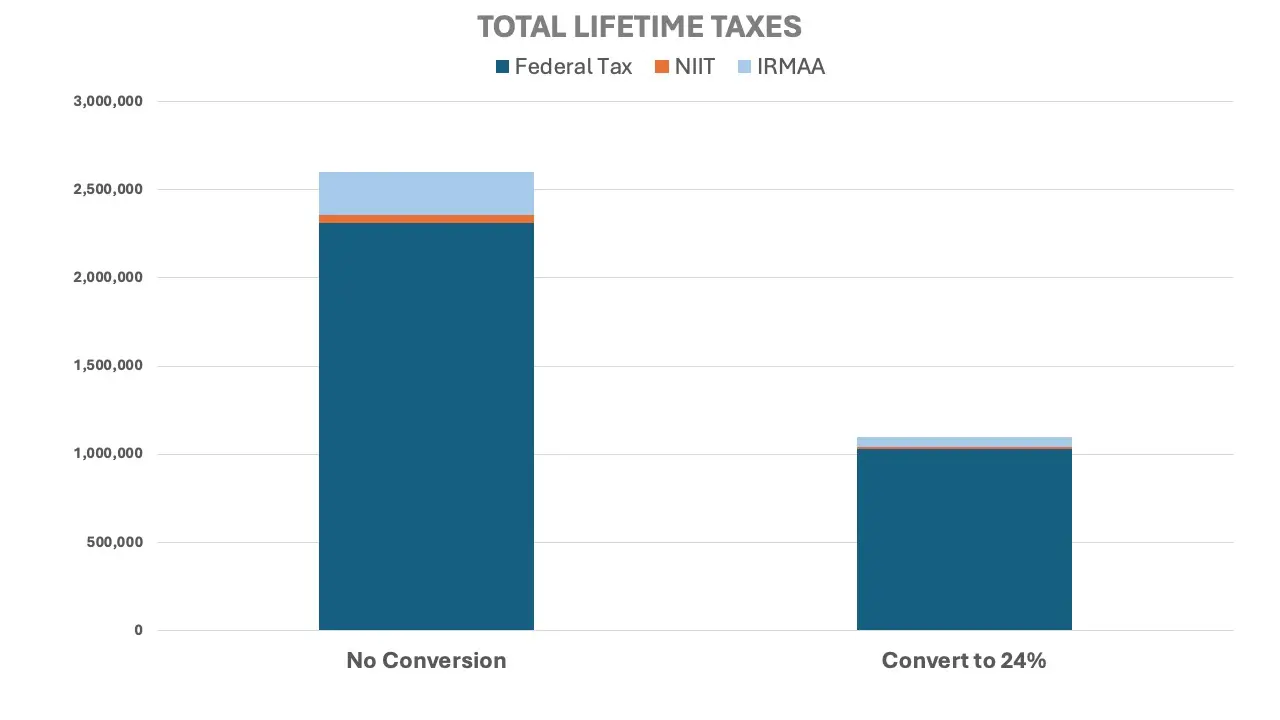

First, Compare Total Lifetime Taxes

The simplest approach is to add up all the projected taxes over the life of the plan. That includes federal taxes, state taxes if applicable, IRMAA, and the Net Investment Income Tax.

Then compare the totals between the no-conversion scenario and the Roth conversion scenario.

This can create a dramatic chart. But by itself, it still may not be all that useful.

Why?

Because simply adding up lifetime taxes does not tell you when the strategy actually becomes more tax efficient.

The timing matters.

If your plan runs to age 95, but the Roth conversion strategy does not become more tax efficient until age 94, that may not feel very attractive.

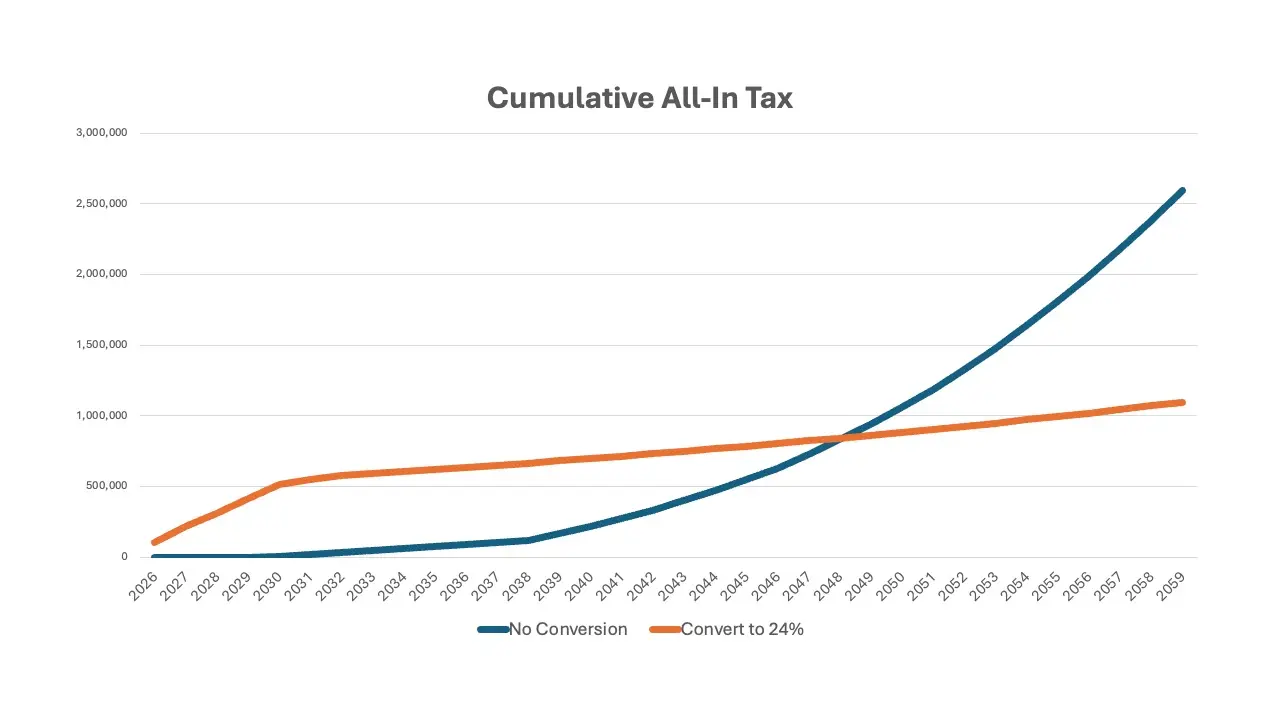

Second, Find the Crossover Point

This is why I prefer to look at the tax burden on a running cumulative basis. This allows us to see the actual crossover point.

The crossover point is the year when the cumulative tax burden of the Roth conversion strategy becomes lower than the cumulative tax burden of the no-conversion strategy.

Roth Conversion Break-Even Point:

The year when cumulative all-in taxes under the conversion strategy become lower than cumulative all-in taxes under the no-conversion strategy.

In one example, converting to the top of the 24% bracket created a higher cumulative tax burden for many years. But eventually, the conversion strategy became more tax efficient, while the cumulative tax burden in the no-conversion scenario continued climbing faster.

That is the type of chart that can change how you think about Roth conversions.

Step 3: Account for the Time Value of Money

But even cumulative taxes are not the full story.

This is where finance people like to use terms like discounted cash flow analysis and present value. But you do not need to get overly technical to understand the core idea.

$1 today is NOT the same as $1 twenty years from now.

Let’s say you owe me $10,000. I give you two choices. You can pay me today, or you can wait 20 years and pay me then. It is still the same $10,000 either way.

Most people would rather wait 20 years.

Why? Because if you keep that money today, you can use it. You can invest it. You can earn interest on it. You can let it compound. In other words, a dollar you keep today has economic value because it has time to grow.

That matters because Roth conversions create the opposite pattern.

The costs happen upfront. You pay taxes today. That means those dollars are no longer invested and compounding for you.

But many of the benefits do not show up until much later in retirement through lower RMDs, lower taxes, and lower Medicare premiums.

So if we want to compare Roth conversion strategies fairly, we cannot simply add up future tax savings and treat them like they are economically identical to dollars paid today.

What Is Discounting?

Discounting is the process of adjusting future dollars to reflect what those dollars are worth in today’s terms.

For example, a tax savings twenty-five years from now may still be valuable. But it is usually not as valuable as saving that same amount today.

This is where a Roth conversion break-even analysis can change dramatically.

What Discount Rate Should You Use?

Once you understand why future dollars should be discounted, the next question is obvious: what discount rate should you use?

This is where things can get surprisingly subjective.

There is no universally correct answer.

The discount rate is really an estimate of what those dollars could have done for you if they had remained invested instead of being used to pay taxes today.

If paying taxes today means pulling money out of a portfolio that might otherwise earn 5% annually, then maybe 5% is a reasonable discount rate.

If you think a more conservative assumption is appropriate, maybe you use 3%.

If you think those dollars could compound more aggressively over long periods of time, maybe you use 7%.

The higher the discount rate, the less valuable future tax savings become in today’s dollars. That tends to make Roth conversions look less attractive because most of the pain happens now, while many of the benefits occur later.

Why Two Smart People Can Disagree

This is exactly why two intelligent people can look at the same Roth conversion analysis and come to completely different conclusions.

They may simply have different assumptions about the value of current dollars versus future dollars.

One person may use a discount rate closer to inflation. Another may use a discount rate closer to expected investment return. Another may care less about lifetime tax savings and more about tax diversification or legacy planning.

None of those perspectives are automatically wrong. They are just different assumptions.

Roth conversion analysis depends heavily on assumptions about:

- Current tax rates

- Future tax rates

- Investment returns

- Inflation

- Life expectancy

- IRMAA exposure

- Net Investment Income Tax exposure

- ACA premium subsidies before age 65

- Widow’s penalty risk

- Charitable giving and QCDs

- Estate planning goals

This is also why people often fall into paralysis by analysis. There is so much information, so many variables, and so many assumptions that they end up doing nothing at all.

Sometimes doing nothing is the right decision. But not always.

Why Tax Savings Alone Is Not Enough

This is why I am not a big fan of using pure tax savings as the primary way to evaluate Roth conversions.

Tax savings matter. But they are only one part of the analysis.

A better question is not simply:

“Will this save taxes?”

A better question is:

“Does this improve my after-tax financial position?”

That is a much more complete question because it considers the entire household balance sheet, not just isolated tax payments.

This is where tax-adjusted portfolio value can be more useful than simply comparing lifetime taxes. A tax-adjusted portfolio view accounts for the fact that a traditional IRA has an embedded tax liability, while a Roth IRA generally does not.

In other words, the goal is not to win a tax-savings contest. The goal is to improve the retirement plan.

Frequently Asked Questions

Do Roth conversions always save taxes?

No. Roth conversions do not always save taxes. Whether they save taxes depends on current tax rates, future tax rates, investment returns, IRMAA exposure, NIIT exposure, spending patterns, life expectancy, and estate planning goals.

What is the Roth conversion break-even point?

The Roth conversion break-even point is the year when the cumulative tax burden under the Roth conversion strategy becomes lower than the cumulative tax burden under the no-conversion strategy.

Should IRMAA be included in Roth conversion analysis?

Yes. IRMAA should usually be included because Roth conversions increase income and may trigger higher Medicare Part B and Part D premiums. Ignoring IRMAA can understate the true cost of a Roth conversion.

Does the Net Investment Income Tax apply to Roth conversions?

A Roth conversion itself is not net investment income. However, because a Roth conversion increases modified adjusted gross income, it may cause more dividends, interest, or capital gains to become subject to the Net Investment Income Tax.

Why does the time value of money matter for Roth conversions?

Roth conversions usually create upfront tax costs while many benefits occur years later. The time value of money matters because dollars paid in taxes today could otherwise remain invested and potentially compound over time.

What discount rate should be used for Roth conversion analysis?

There is no universally correct discount rate. Some people may use an inflation rate. Others may use a conservative return assumption, an expected portfolio return, or an after-tax expected return. The right rate depends on what you believe those dollars could have done if they had not been used to pay taxes today.

Why can two advisors disagree about Roth conversions?

Two advisors may use different assumptions about future tax rates, investment returns, discount rates, IRMAA, life expectancy, estate planning goals, and survivor tax brackets. Those differences can lead to very different conclusions.

What is a better metric than lifetime tax savings?

Lifetime tax savings can be useful, but it should not be the only metric. A tax-adjusted portfolio value may be more useful because it considers the after-tax value of the household’s assets rather than focusing only on taxes paid.

Want Help Evaluating Roth Conversions?

If you want help determining whether Roth conversions improve your long-term after-tax financial position, schedule a Retirement Clarity Meeting.

Schedule a Retirement Clarity Meeting