Medicare Premiums Could Double Over the Next Decade. Here’s What Retirees Need to Know

May 25, 2026

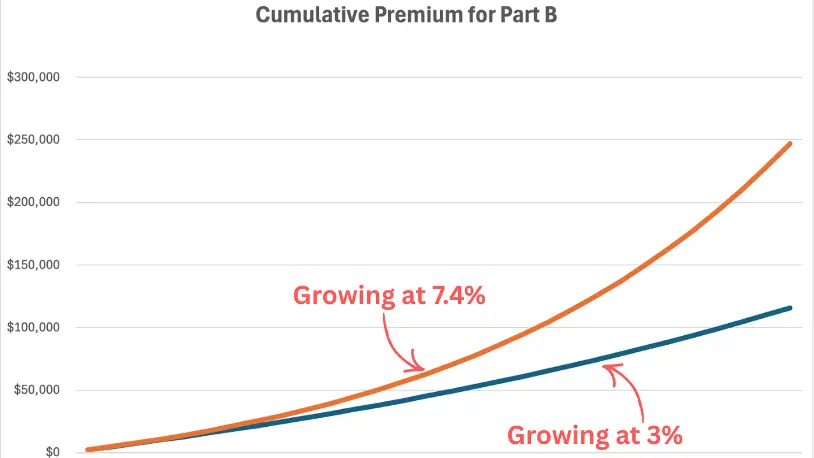

A recent Senate report projects that Medicare Part B premiums could nearly double over the next 10 years. Specifically, annual premiums are expected to rise from around $2,400 today to roughly $5,000 by 2035. That works out to an annual growth rate of approximately 7%.

At first glance, that may not sound catastrophic. But when you stretch those increases across a 25- or 30-year retirement, the numbers become significant.

For the average retiree, this could mean spending an additional $130,000 on Medicare premiums throughout retirement. For married couples, the added cost could exceed $260,000. And for retirees subject to IRMAA surcharges, the impact could be substantially higher.

The bigger issue is not one dramatic increase. It is the slow, steady compounding effect of healthcare costs rising faster than many retirement plans anticipate.

Why Medicare Premiums Keep Rising

Most retirees assume their Medicare premiums are tied primarily to their personal healthcare usage. But that is not how Medicare Part B works.

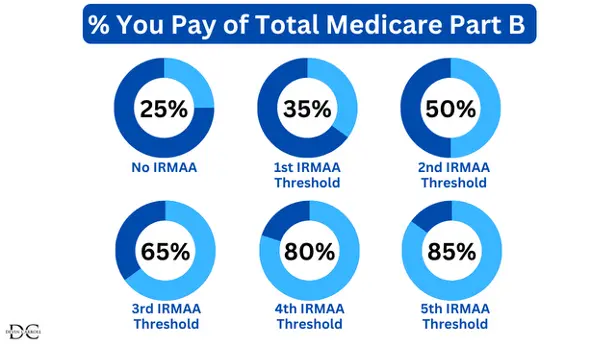

By law, Medicare Part B premiums are designed to cover roughly 25% of the total cost of the Medicare Part B program. The remaining 75% is funded through general tax revenue.

That means your premium is not based solely on your own healthcare expenses. Instead, it is tied to the overall cost of the entire Medicare system.

Think of it like this: everyone’s healthcare costs go into one large pool, and Medicare calculates premiums based on the total expense of the program. When total program costs rise, premiums rise too.

And right now, those costs are increasing faster than they have historically.

Some of that is simply due to healthcare inflation. But another major factor involves how Medicare Advantage plans are funded.

Traditional Medicare vs. Medicare Advantage

To understand what is happening, it helps to understand the difference between Traditional Medicare and Medicare Advantage.

Traditional Medicare is the original Medicare program. The government pays doctors and hospitals directly for the healthcare services you receive.

Medicare Advantage works differently. Instead of paying providers directly, the government pays private insurance companies a fixed amount to manage your care. These plans still provide Medicare Part A and Part B benefits, and they often include additional features like prescription drug coverage, dental, vision, and other supplemental benefits.

From the retiree’s perspective, both systems provide healthcare coverage. But financially, the government is still paying for your care either way.

And according to the Senate report referenced in the video script, the government currently spends about 20% more on average for someone enrolled in Medicare Advantage compared to someone in Traditional Medicare.

That higher spending increases the overall cost of the Medicare system, which then feeds back into higher Part B premiums for everyone, regardless of which type of Medicare coverage they use.

Why IRMAA Makes This More Important for Higher-Income Retirees

If you are subject to IRMAA (Income-Related Monthly Adjustment Amount), the impact can be even more significant.

Most retirees pay approximately 25% of the total Part B program cost through their premiums. But IRMAA increases that percentage based on income.

In other words, rising Medicare costs do not affect everyone equally.

The more taxable income you generate in retirement, the more exposed you may be to rising healthcare costs.

The Real Risk Is Underestimating Healthcare Inflation

Most retirement plans already account for healthcare inflation to some degree. The problem is that many assumptions may simply be too low.

A lot of retirement projections use long-term inflation assumptions closer to 3%. But if Medicare-related costs rise closer to 7% annually, that creates a large gap over time.

It is not the kind of expense increase that suddenly destroys a retirement plan overnight. Instead, it gradually erodes spending flexibility over decades.

And that is exactly why healthcare costs deserve stress testing inside a retirement plan.

How Retirees Can Prepare for Rising Medicare Costs

The goal is not to perfectly predict future Medicare premiums. No one can do that.

The goal is to build flexibility into your retirement income plan so that rising costs do not create unnecessary strain later.

One of the biggest planning opportunities is gaining greater control over taxable income in retirement.

That is where strategies like Roth conversions can become valuable. Roth conversions are not just about reducing future taxes. They can also help retirees manage income levels later in retirement, which may reduce exposure to IRMAA surcharges and rising Medicare costs.

The more flexibility you have over where your retirement income comes from, the more control you have over how much of these Medicare increases you actually feel.

The Bigger Retirement Planning Question

At the end of the day, the key issue is not whether Medicare premiums will rise.

The structure of the system makes continued increases likely. The more important question is:

How exposed are you to those increases?

You cannot control where Medicare premiums go. But you can control how your retirement income is structured, how taxes are managed, and how flexible your plan is over time.

That is why this may be a good time to revisit your retirement assumptions, especially around healthcare costs and taxable income planning.

Because retirement risks are often not the dramatic events people fear most. Sometimes they are the slow-moving costs that compound quietly for decades.