A Roth Conversion That Saved $460,000 in Taxes…But Left Them With Less Money

May 28, 2026

Most people evaluate Roth conversions the same way.

They run an analysis, compare lifetime taxes with and without conversions, and if the conversion strategy shows lower taxes, they assume it’s automatically the better decision.

But that assumption can lead retirees in the wrong direction.

I recently reviewed a case where a Roth conversion strategy reduced a couple’s projected lifetime tax bill by nearly $460,000. On paper, it looked like a huge win.

But when we dug deeper, the strategy actually left them with less after-tax wealth over time.

That sounds impossible at first. If you save almost half a million dollars in taxes, shouldn’t you end up with more money?

Not necessarily.

Because when it comes to Roth conversions, it’s not just about how much tax you pay. It’s also about when you pay it. And that timing can dramatically affect compounding over decades.

The Scenario

This couple was 62 years old and lived in California, so both federal and state income taxes mattered.

They had:

- $3 million in pre-tax retirement accounts

- $500,000 in a brokerage account

- Expected Social Security benefits of approximately $5,700 per month starting at age 67

- A retirement spending need of $12,000 per month after taxes

Like many retirees, they wanted to know whether Roth conversions could reduce their lifetime tax burden.

Their retirement planning software showed that if they converted enough each year to fill up the 22% tax bracket between ages 62 and 67, they could reduce lifetime taxes by more than $460,000.

At first glance, that seems like an obvious decision.

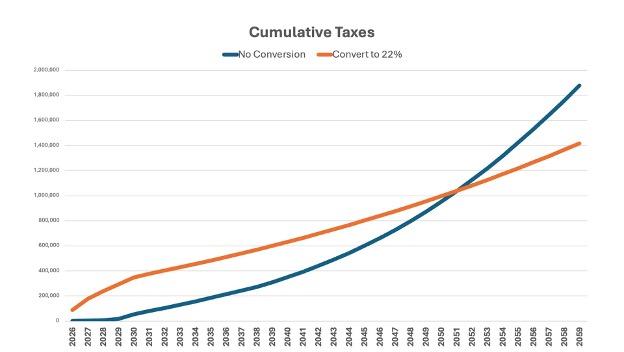

The cumulative tax projections looked great. Early on, taxes were significantly higher because of the conversions, but eventually the strategy broke even around age 87. After that, the tax savings accelerated meaningfully.

The Roth conversion strategy reduced projected lifetime taxes by more than $460,000, which initially made the strategy appear superior.

And this is where many Roth conversion analyses stop.

But that’s also where the analysis can start to break down.

Minimizing Taxes Is Not the Same as Maximizing Wealth

A lower lifetime tax bill does not automatically mean a better financial outcome.

That distinction matters.

When retirees focus only on cumulative taxes, they can miss a much more important question:

After taxes are paid, how much of the portfolio is actually available to spend?

That’s where we shifted the analysis.

Instead of only looking at cumulative taxes, we evaluated the couple’s tax-adjusted portfolio.

In simple terms, a tax-adjusted portfolio estimates what the portfolio is worth after accounting for future taxes. It attempts to answer the question:

“How much of this money is actually mine?”

Because a $1 million Roth IRA is not the same as a $1 million traditional IRA.

The traditional IRA still carries a future tax liability. The Roth IRA does not.

So we compared the couple’s projected after-tax wealth under two strategies:

- No Roth conversions

- Roth conversions up to the 22% bracket until age 67

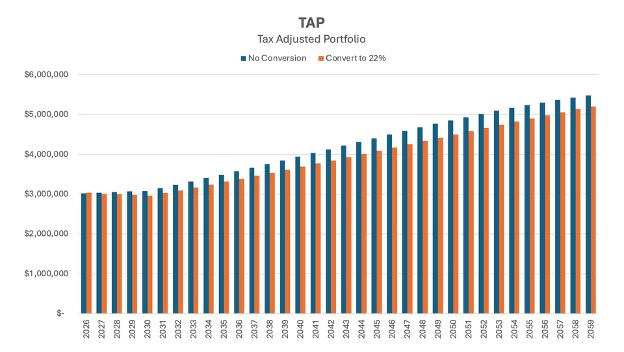

And surprisingly, the Roth conversion strategy produced a lower tax-adjusted portfolio over time.

The gap started small but widened gradually over the years. Even though the couple was paying less tax overall, they were ending up with less spendable wealth.

Despite lower lifetime taxes, the Roth conversion strategy resulted in a lower after-tax portfolio over time.

So what happened?

The Hidden Cost of Roth Conversions: Lost Compounding

The answer comes down to compounding.

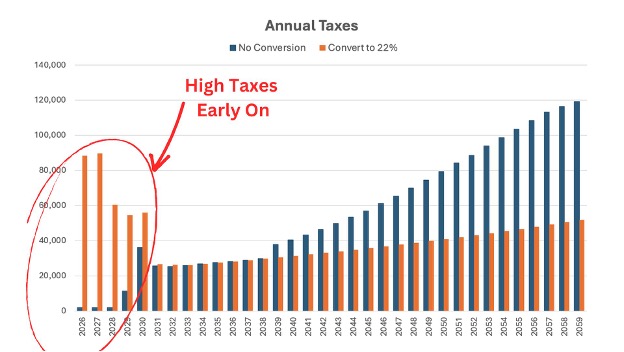

Large Roth conversions create significantly higher taxes in the early years of retirement.

That means large amounts of money leave the portfolio decades earlier than they otherwise would have.

And once those dollars leave the portfolio to pay taxes, they no longer have the opportunity to compound.

That’s the key issue many retirees miss.

Without Roth conversions, taxes typically stay relatively low early in retirement. Then later, once required minimum distributions (RMDs) begin, taxes rise sharply.

That future spike in taxes is exactly what many people are trying to avoid.

But Roth conversions essentially reverse the timeline:

- Higher taxes now

- Lower taxes later

The problem is that paying taxes earlier can reduce the portfolio’s long-term growth potential.

Those tax payments reduce the amount of money left invested during the years where compounding matters most.

Suggested Caption:

Large Roth conversions created substantially higher taxes in the early years, reducing the amount of money left invested and compounding for future growth.

And over long periods of time, compounding matters enormously.

Even if future taxes are lower, the portfolio may never fully recover from the lost growth on those dollars that left early.

That’s why the tax-adjusted portfolio never caught up in this case.

Why This Doesn’t Mean Roth Conversions Are Bad

This is not an argument against Roth conversions.

In fact, there were still several very good reasons this couple wanted to convert money to Roth accounts.

For example, they wanted to protect against the widow’s penalty.

When one spouse dies, the surviving spouse often ends up filing as single while maintaining a similar income level. That can push the survivor into significantly higher tax brackets later in life.

Roth assets can help reduce that future tax burden.

They also had one child who was a high earner and would likely inherit any remaining retirement accounts. Since inherited traditional IRAs generally must be distributed within 10 years, leaving behind a large pre-tax account could force their child to recognize substantial taxable income during peak earning years.

Roth accounts can be much more favorable for heirs in that situation.

So the issue wasn’t whether Roth conversions were “good” or “bad.”

The issue was that the original strategy was too aggressive.

Once we refined the conversion plan and looked beyond just lifetime tax savings, we were able to create a more balanced approach.

The Real Goal of Roth Conversions

Many retirees unintentionally optimize for the wrong metric.

They focus entirely on minimizing taxes.

But the goal of retirement planning is not to pay the lowest lifetime taxes possible.

The goal is to maximize what you keep.

And those are not always the same thing.

A Roth conversion strategy should account for:

- Future tax rates

- RMD exposure

- Widowhood risk

- Legacy goals

- Heirs’ tax situations

- Portfolio compounding

- Spending needs

- Longevity

- State taxes

- Medicare IRMAA surcharges

Tax savings are only one piece of the puzzle.

The broader question is whether the strategy improves your overall after-tax financial outcome.

Because sometimes, paying less tax over your lifetime can still leave you with less money in the end.