The Worst Ages to File for Social Security

Mar 02, 2026

We often hear about the best age to file for Social Security, but hardly anyone talks about the worst ages to file. And knowing what these ages are can be really important before you make your filing decision.

Most people know your benefit gets bigger the longer you wait, but what surprises a lot of people is that not every year pays off the same. For example, before your full retirement age, your benefit will increase by just 6.7% one year, but 8.3% the next. And even after full retirement age, it can increase by 8% one year, but only 6.9% later.

In this article, I am going to show you exactly which ages give you the smallest benefit increases, and if those increases matter to you, why those might be the worst ages to file for Social Security.

Sometimes Knowing What You Do Not Want Helps

I think it is worth pointing out that sometimes, you do not really know what you want until you know what you do not want. The process of elimination can make certain decisions a lot clearer.

And that is exactly what this next part can do. When you see the numbers laid out year by year, it becomes easier to spot which filing ages might not make sense for you, and which ones could be worth waiting for.

How Social Security Increases and Decreases Actually Work

But before we get into the increases for delaying, it is really important to understand how the age based decreases or increases around your full retirement age actually work. This is where all the math is rooted, and it is also where a lot of the misunderstandings come from about how those increases between age 62 and 70 really work.

So let us start by looking at a chart that many of you are already familiar with. For this example, we will assume a full retirement age of 67 and a monthly benefit of $3,000 at that age. If you file early, your benefit will be reduced, all the way down to about $2,100 at age 62. And if you wait past full retirement age, your benefit will increase each year until age 70, where it would reach about $3,720 per month.

Now, I do not want to get too far into the weeds here, but it is important to understand how these increases and decreases are actually calculated, because that will make the numbers we look at later make a lot more sense. If you file at your full retirement age, you will receive 100% of your benefit. In the three years before that, your benefit is reduced by five ninths of one percent for every month you file early. Over the course of a year, that adds up to about a 6.7% reduction.

For anything beyond those three years, in this case ages 62 and 63, your benefit is reduced by five twelfths of one percent per month, which works out to about 5% per year. Then, once you are past full retirement age, your benefit increases by two thirds of one percent for every month you delay, which equals about an 8% increase per year.

Why the Math Looks Uneven

Now, one thing that often confuses people is how these increases and decreases are applied. They are not compounding. They are stacking.

Here is what that means. Each month’s increase or decrease is based on your full retirement age benefit, not on the new number after the last adjustment. So if your full retirement benefit is $3,000, every percentage change is calculated from that $3,000 base. It does not grow on top of itself like investment returns would.

That is why the math does not work the way a lot of people expect, and it is exactly why the year to year changes look uneven when we chart them out.

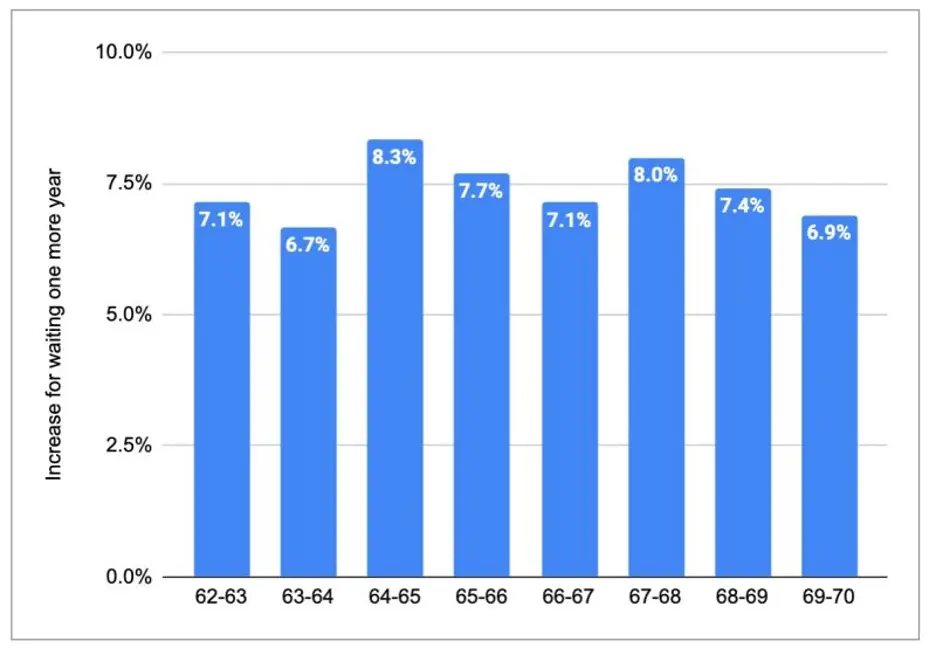

The Year by Year Increases

Now let us look at the year over year increases that start at age 62. We usually talk about Social Security in terms of how much your benefit goes down if you file early. But it can be really helpful to flip that around and ask, how much will my benefit increase if I wait one more year.

And this is where the math starts to get a little surprising.

Here is what those increases actually look like year by year:

• Between ages 62 and 63, your benefit goes up by about 7.1%. • From 63 to 64, it is only 6.7%. • From 64 to 65, it jumps all the way to 8.3%, which is the biggest increase on the chart. • From 65 to 66, it is 7.7%, and from 66 to 67, it is 7.1%. • From 67 to 68, there is another strong bump of 8.0%. • Finally, it is 7.4% from 68 to 69, and 6.9% from 69 to 70.

So even though most people think their benefit just grows evenly every year, this breakdown shows that some years give you a lot more value for waiting than others.

The Ages With the Smallest Increases

Now, when you look at this chart, something interesting jumps out. If your goal is to get the most growth for waiting, there are a few years that do not really pull their weight.

Those are the years where your benefit grows the least from one year to the next, specifically ages 63 to 64, where the increase is just 6.7%, and 69 to 70, where it is 6.9%.

So if you are thinking, maybe I will just wait one more year, these are the years where that extra wait gives you less of a bump compared to others.

That does not mean filing at those ages is a bad decision. There are plenty of personal factors that matter more, and the reality is that there is no single factor that should be the reason you file at a certain age.

Things like spousal benefits, survivor benefits, taxes, how your accounts are structured, and your need for income all play a role, along with a whole laundry list of other considerations.

But data points like the ones we have talked about today can help make the trade offs easier to understand. When you can see the year by year increases laid out clearly, especially when paired with a visual chart, it becomes easier to understand the trade offs involved in waiting or filing earlier.

Ultimately, there is no single right age to file for Social Security. But understanding which years give you the smallest benefit increases can help you ask better questions, weigh your options more confidently, and make a decision that fits your broader retirement plan.