How Roth Conversions Can Help Protect a Surviving Spouse From the Widow’s Penalty

May 20, 2026

One of the biggest reasons retirees tell me they’re interested in Roth conversions has nothing to do with lowering their own taxes today.

It’s about protecting the surviving spouse.

More specifically, it’s about avoiding what’s often called the widow’s penalty.

This is one of the most overlooked tax problems in retirement planning, and for couples who have accumulated large traditional IRA balances, it can create a painful situation where household income falls after the death of a spouse… but taxes go up.

And unfortunately, this tends to happen at the exact moment the surviving spouse is already dealing with enough emotionally.

In this article, I want to walk you through a real retirement planning case study that shows exactly how the widow’s penalty works, why it happens, and how Roth conversions can potentially reduce the impact.

What Is the Widow’s Penalty?

When one spouse dies, the surviving spouse eventually moves from filing taxes as Married Filing Jointly to filing as a Single taxpayer.

That matters because the tax system changes dramatically for a single filer.

The tax brackets become much smaller.

The standard deduction shrinks.

Medicare IRMAA thresholds are cut in half.

But in many cases, retirement income does not fall nearly as much as people expect.

The result is that one surviving spouse can end up paying significantly more taxes on less income.

That’s the widow’s penalty.

Note: See the current tax brackets, standard deductions, and Medicare premiums at my retirement reference page.

A Real Retirement Planning Example

Let me show you an example.

This couple was both 62 years old when we ran this analysis. They had:

- $900,000 in a traditional IRA

- $250,000 in a brokerage account

- Social Security benefits of $3,600 per month for one spouse

- Social Security benefits of $1,800 per month for the other spouse

Their retirement income goal was:

- $8,000 per month after taxes while both spouses were alive

- $6,400 per month after taxes if one spouse died

In other words, they assumed spending would decrease by roughly 20% after the first death.

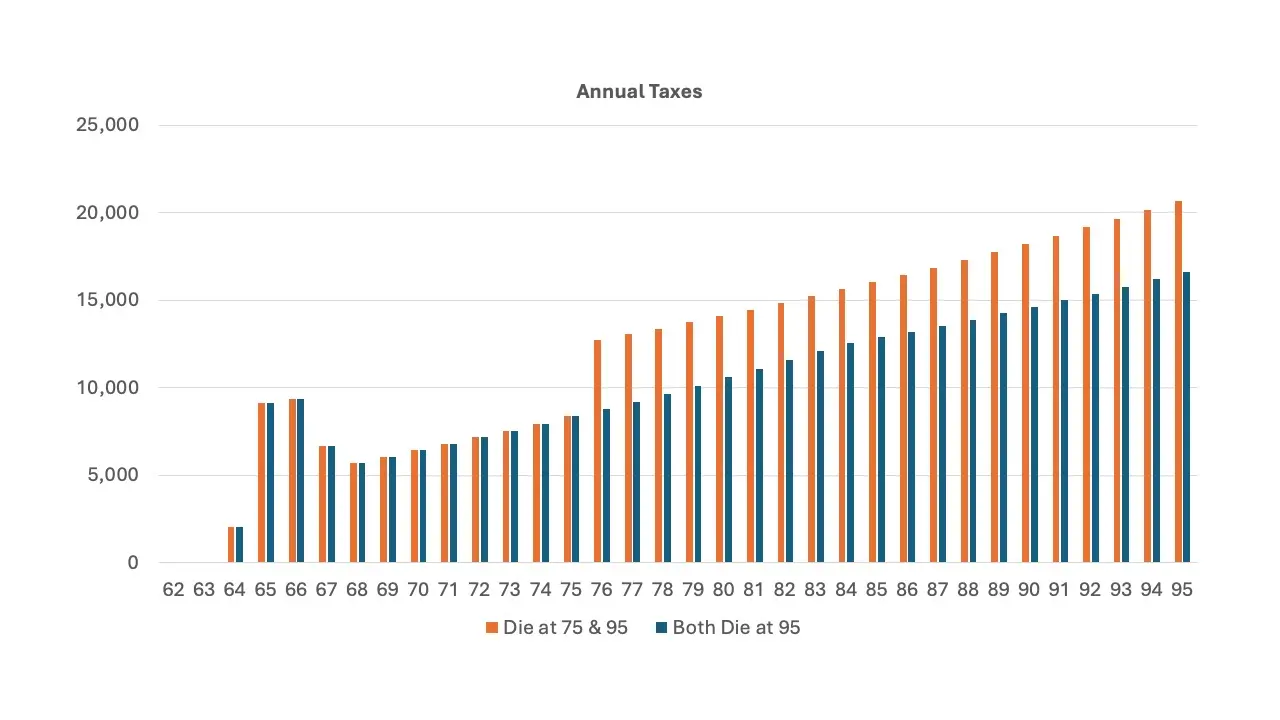

We tested two different scenarios:

- Both spouses live to age 95

- One spouse dies at age 75 while the surviving spouse lives to 95

The goal was to see how much additional tax burden the surviving spouse would face.

What Happened to Taxes After the First Death?

When we compared the two scenarios, the difference became obvious very quickly.

In the scenario where both spouses lived to 95, taxes gradually increased over time, but there were no major spikes.

But in the scenario where one spouse died at age 75, the annual tax bill jumped sharply beginning the very next year.

And here’s what makes this so surprising:

Total household income was actually lower after the death.

One of the Social Security checks disappeared.

But taxes still increased.

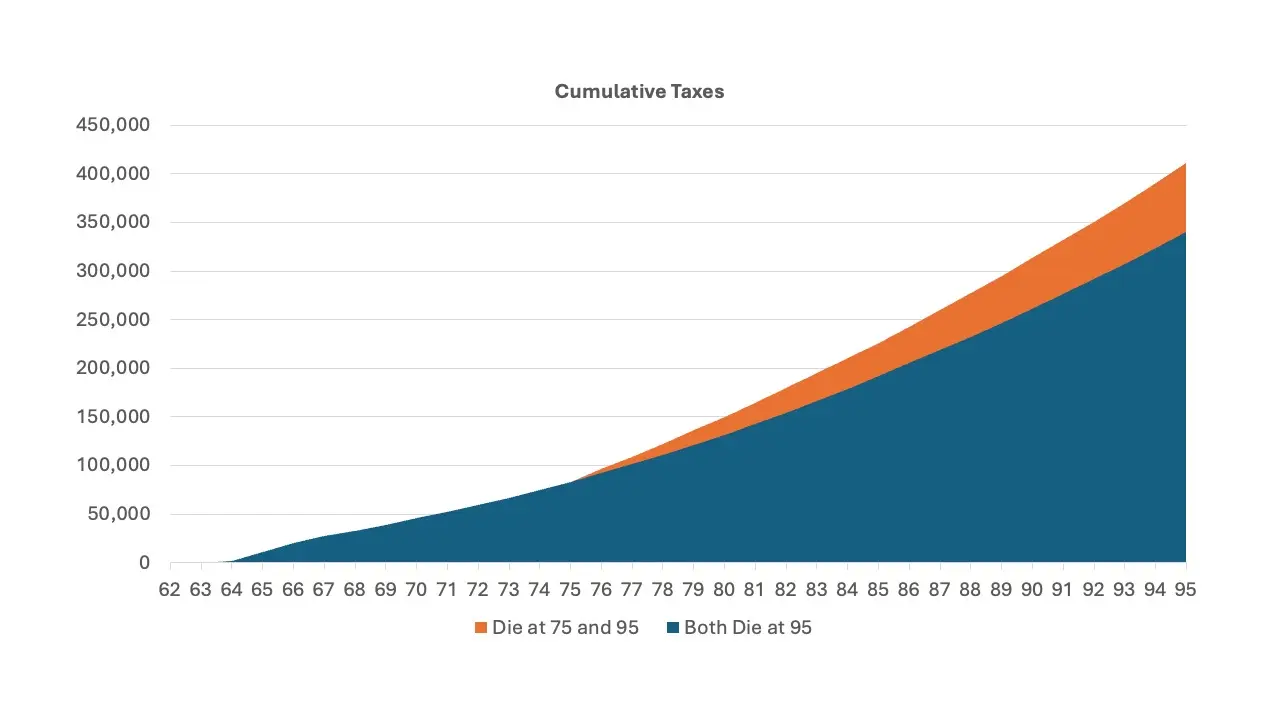

When we looked at cumulative taxes paid over the remainder of retirement, the surviving spouse scenario consistently paid more in taxes year after year.

Why Taxes Can Increase Even When Income Drops

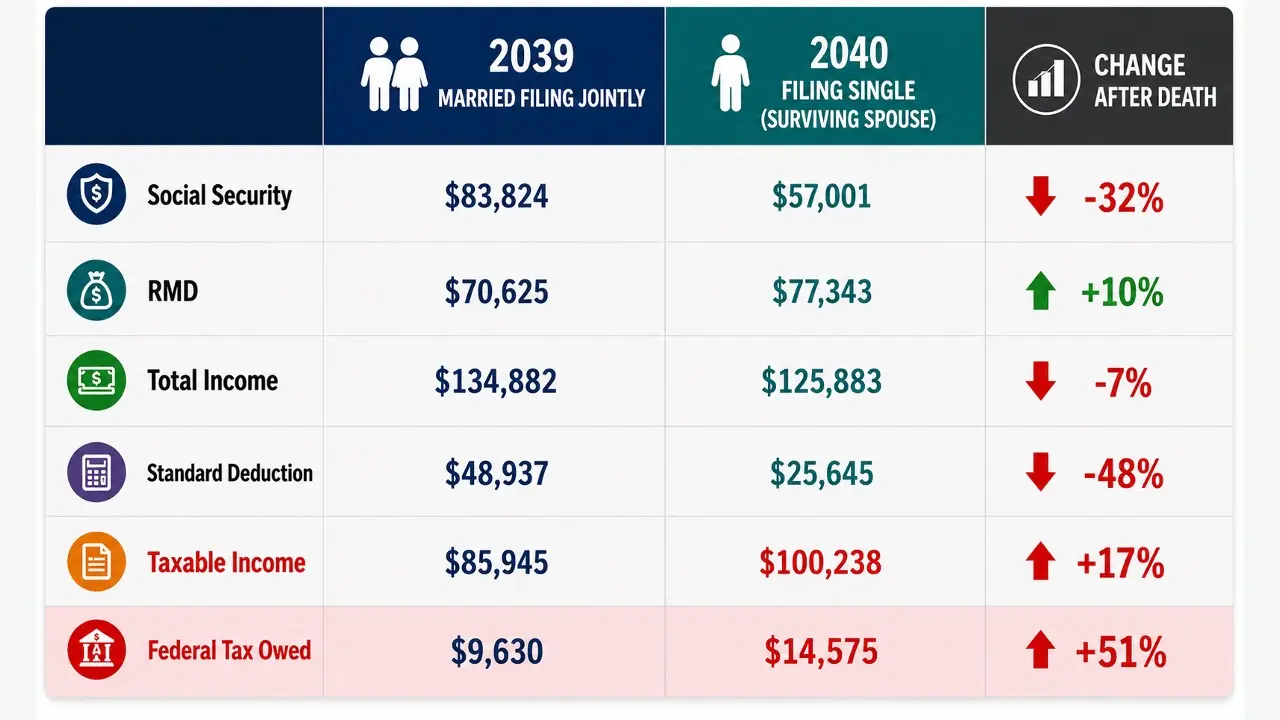

To really understand why this happens, it helps to zoom in on the exact year the filing status changed.

In this case, we compared:

- 2039: Married Filing Jointly

- 2040: Filing Single as the surviving spouse

Here’s what happened:

Social Security Income Dropped

Because the surviving spouse receives the greater of the two Social Security benefits, the smaller benefit disappeared.

That caused total Social Security income to fall by about 32%.

The IRA Did Not Disappear

The surviving spouse inherited the IRA and continued taking Required Minimum Distributions from the same account.

In fact, the RMD actually increased slightly.

Total Income Barely Changed

Even though one Social Security benefit disappeared, total household income only declined by about 7%.

The Standard Deduction Was Nearly Cut in Half

This is where the widow’s penalty really showed up.

The standard deduction dropped dramatically when the surviving spouse switched from Married Filing Jointly to Single.

As a result:

- Taxable income increased by 17%

- Federal taxes owed increased by 51%

That’s the widow’s penalty in action.

Income went down.

Taxes went up.

How Roth Conversions Can Help

A Roth conversion is not the only strategy available for managing the widow’s penalty, but in many cases it can be one of the most effective.

The basic idea is fairly simple:

You intentionally move money from traditional IRAs into Roth IRAs during years where your tax bracket is relatively low.

You pay taxes now at known rates in exchange for reducing future taxable Required Minimum Distributions.

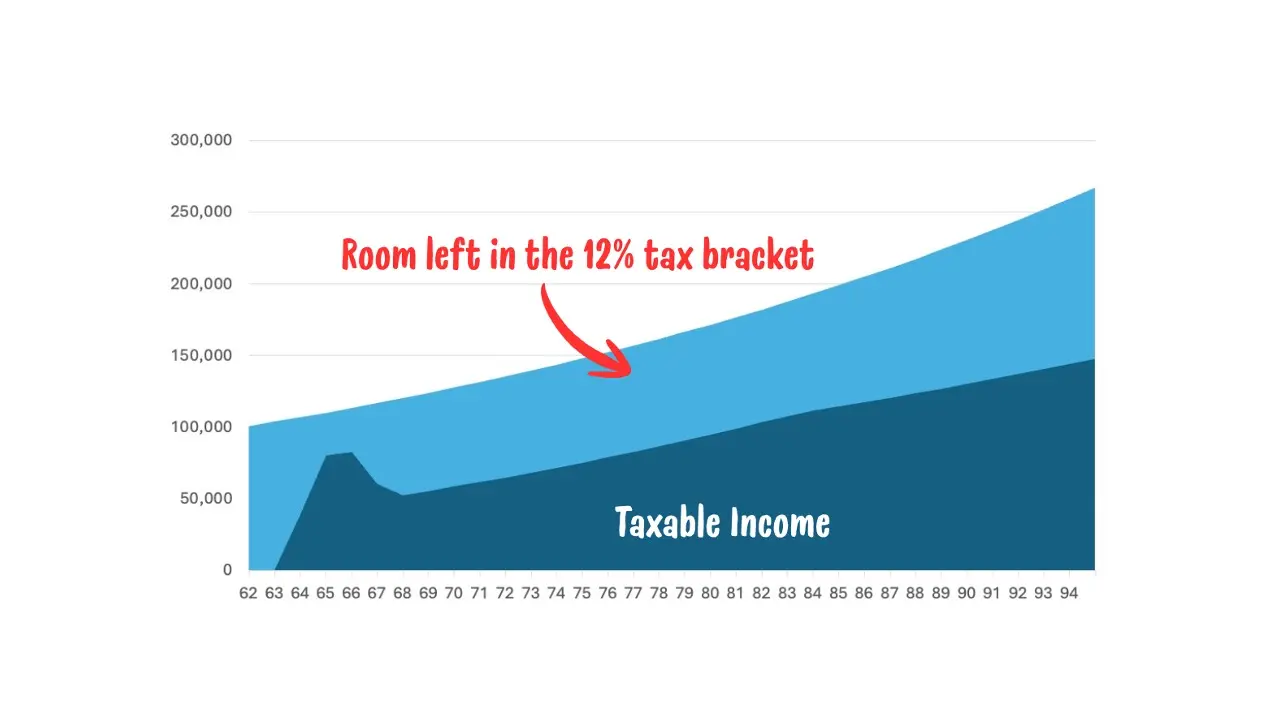

For this particular couple, the strategy opportunity was very clear.

When we looked at their projected taxable income during the early retirement years, there was substantial room left inside the 12% tax bracket.

That gave them the opportunity to do meaningful Roth conversions at relatively low tax rates before:

- Required Minimum Distributions increased

- One spouse potentially passed away

- Filing status changed to Single

By reducing future IRA balances ahead of time, the surviving spouse would eventually have:

- Lower RMDs

- Lower taxable income

- More tax-free Roth assets available for spending

- Greater flexibility later in retirement

Roth Conversions Are Not One-Size-Fits-All

Now with all that said, Roth conversions are not automatically the right answer.

And this is where a lot of online discussions about Roth conversions become overly simplistic.

There is rarely one perfect piece of evidence that proves beyond a shadow of a doubt that a Roth conversion is the correct decision.

The right strategy depends on a long list of factors, including:

- Current tax brackets

- Future income expectations

- IRA balances

- Age

- Health

- Legacy goals

- Charitable intentions

- State taxes

- Medicare IRMAA thresholds

- Spending flexibility

But perhaps most importantly, Roth conversions are not just about minimizing taxes.

They’re often about protecting against a future risk.

In this case, the risk was that the surviving spouse could face a much larger tax burden later in life while also navigating the emotional difficulty of losing a spouse.

Roth Conversions Aren't Just About Taxes

The widow’s penalty is real.

And for retirees with large traditional IRA balances, it can create a surprising and frustrating outcome where taxes increase after the death of a spouse even though household income declines.

That does not automatically mean everyone should rush out and do Roth conversions.

But it does mean this issue deserves careful planning.

A thoughtful Roth conversion strategy during the early retirement years can potentially:

- Reduce future Required Minimum Distributions

- Lower future taxable income

- Create more flexibility for the surviving spouse

- Reduce long-term tax exposure

- Help avoid large spikes in taxes later in retirement

The important piece is understanding what problem you’re trying to solve.

Because ultimately, Roth conversions are not just a tax strategy.

They’re a planning tool designed to help retirees create more flexibility, reduce future risks, and protect the people they care about most.